The Hundred-Million-Dollar Charity With Nobody Working There

The numbers tell their own story. Of the $102.7 million that came in, $101.98 million went out. The organization retained about $721,000, seven-tenths of one percent, and ended 2024 holding $324,050 with no liabilities and no staff.

There is a temptation, when a name like Neville Roy Singham enters the picture, to reach immediately for the largest story available. China. State propaganda. Foreign influence laundered through American nonprofits and routed back into American politics. That story is real, it is being chased by Congress and by federal agencies, and it is contested, slow, and years from resolution.

Sam Antar is not chasing that story. He is chasing the tax returns.

Antar is a forensic accountant, and before that, he was a criminal. He was the chief financial officer of Crazy Eddie, the electronics chain that became one of the most notorious securities frauds of the 1980s, and he helped engineer it. Then he cooperated with the government and spent the next three decades teaching the FBI, the SEC, and the Justice Department how men like the one he used to be cook the books. He knows where the bodies are buried because he buried some of them himself.

So when Antar looks at the Singham network, he does not look for the dramatic thing. He looks for the provable thing. And in a new investigation published at WhiteCollarFraud.com, he has found it sitting in plain sight, on documents the organizations themselves signed under penalty of perjury.

One charity in that network reported moving more than $100 million out of the United States. It had zero employees.

The Oldest Lesson in Enforcement

Antar's framing is the discipline of his trade, and it is worth stating plainly because it is what separates this report from the noise around it. You do not have to prove anything about China to ask whether a charity followed the Internal Revenue Code. That question gets answered line by line, on filings that are public to anyone with an internet connection.

It is the oldest lesson in white-collar enforcement. Al Capone was not convicted of murder. He was convicted of tax evasion. The case you can actually prove is rarely the cinematic one. It is the bookkeeping.

The chain Antar lays out has three points, and they are not complicated.

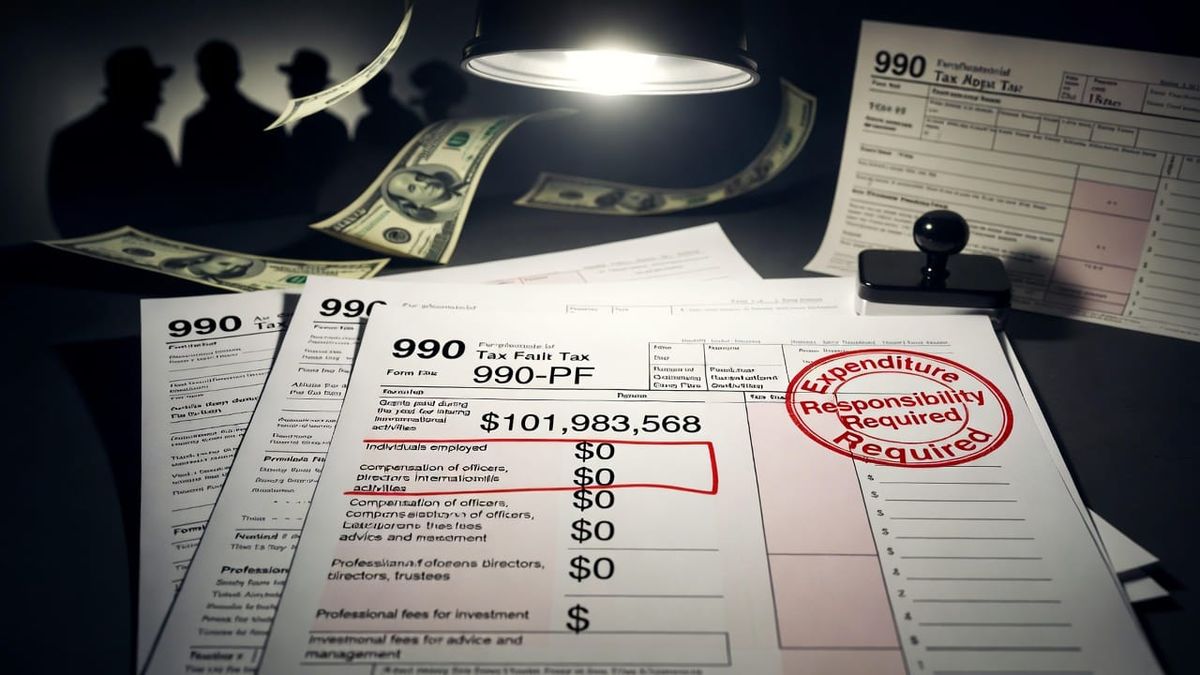

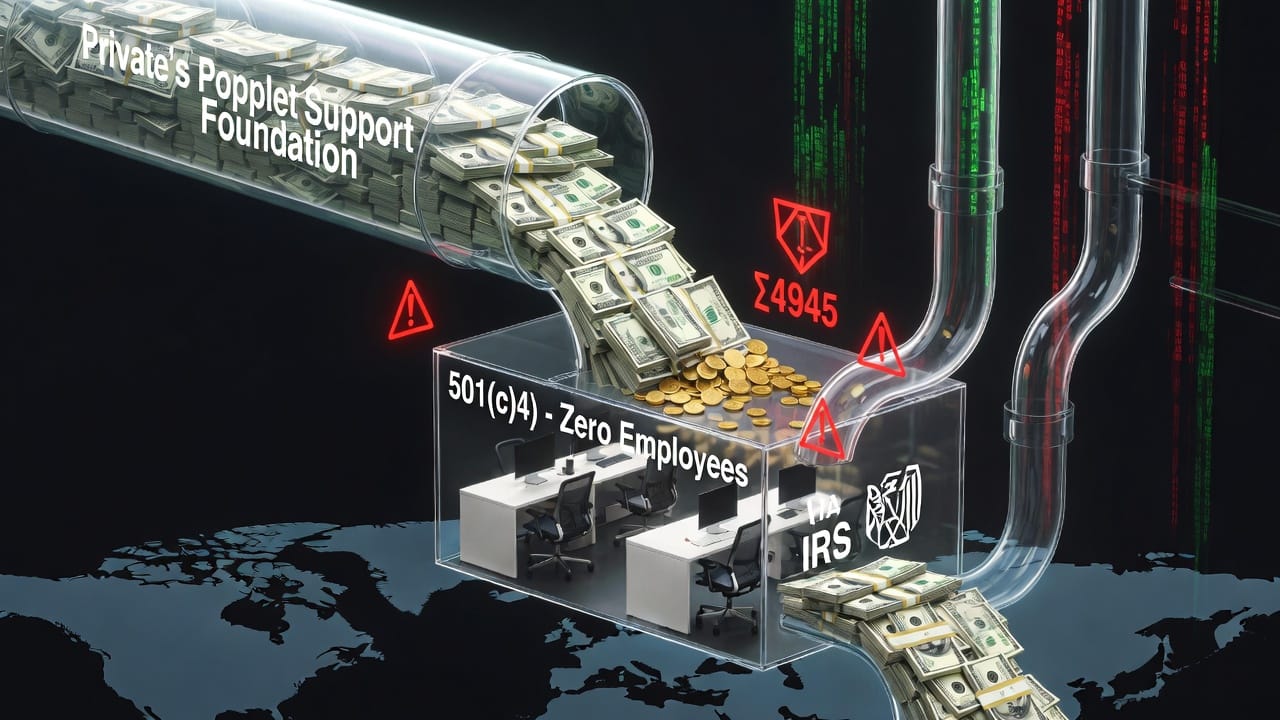

At the top sits People's Support Foundation Limited, a §501(c)(3) private foundation. Between fiscal years 2019 and 2024, according to the foundation's own Form 990-PF filings, it transferred $73,731,279 to two §501(c)(4) social welfare organizations: People's Welfare Association and United Community Fund.

People's Welfare Association then reported moving $101,983,568 in grants abroad over the same period. It reported zero employees. Zero officer pay. Nothing in the professional-fee categories where the cost of administering or monitoring that money would naturally appear.

That is the whole structure. Money in at the top, money out the bottom, and in the middle an organization that, on the face of its own returns, had nobody working there to account for any of it.

Why the Empty Payroll Is the Story

Here is where Antar's expertise earns its keep, because the significance of an empty payroll is not obvious to a layman, and it is the entire case.

When a private foundation gives money to a public charity, the law treats the gift as routine. When a private foundation gives money to a §501(c)(4) — a social welfare organization that is permitted to do things, including political activity, that a charity cannot — the law stops treating it as routine. Internal Revenue Code §4945 requires the foundation to exercise what is called "expenditure responsibility": written grant agreements, monitoring of how the money is actually spent, and reports back from the recipient confirming where it went. Skip that work and the grant becomes a "taxable expenditure," and the foundation owes excise tax.

This is not a gray area the foundation might have stumbled into. Antar establishes that both recipients were §501(c)(4) organizations from their very first filed returns. There was no earlier period as a public charity, no conversion, no moment when a grant to them would have been clean without the monitoring. From the first dollar to the last, the §4945 duty attached.

And the foundation knew it. This is the detail that elevates the report from accounting to indictment.

On its own 2024 Form 990-PF, People's Support Foundation Limited classified both recipients as "noncharitable" in three separate IRS-designated places on the same return. On that same page, it correctly coded other recipients — The People's Forum, The Justice and Education Fund — as "public charity." The foundation demonstrably knew the difference between the two categories. It used both labels on one document. And it deliberately placed these two organizations in the noncharitable column, the column that triggers the strict monitoring rules.

So somebody, somewhere, was obligated to vet these grants, paper the agreements, and confirm where $101 million went. That work costs money. Real money. It shows up on a tax return — on the compensation lines if staff did it, in the professional-fee categories if it was outsourced.

People's Welfare Association reported $0 in every one of those categories, in every one of the six years. No management fees. No consulting. No monitoring of any kind. Roughly $455,000 in total professional services across six years against $101,983,568 in throughput — about 0.45 percent, an amount Antar shows is consistent with nothing more than annual return preparation and routine legal review.

The numbers tell their own story. Of the $102.7 million that came in, $101.98 million went out. The organization retained about $721,000 — seven-tenths of one percent — and ended 2024 holding $324,050 with no liabilities and no staff. That is not the financial profile of an organization running its own programs. It is the fingerprint of a pass-through pipe.

Closing the Escape Hatch

The obvious objection writes itself, and Antar gets there before the reader does. Maybe the foundation paid for the oversight. The duty belongs to the foundation, after all, not the grantee, so the place to look for the monitoring cost is the foundation's return.

The foundation did report substantial professional fees — between roughly $540,000 and $617,000 a year. There, a skeptic could say, is the money that paid for it.

Except the foundation's own required schedules say what that money bought. Every year, the spend is identified as investment management — the cost of managing the foundation's endowment, not of monitoring its grants. The named contractors are described as investment management, legal, accounting, or consulting. Not one is identified with the expenditure-responsibility function the law requires.

So the objection collapses. At neither end of the chain does the public record show a single dollar spent on the oversight the Internal Revenue Code demands. The grantee reported $0 in every category it would occupy. The foundation attributed its fees to managing its investments.

And the thing the monitoring exists to prevent was happening downstream the entire time. People's Welfare Association's Schedule C discloses $15,017,020 in political contributions to §527 organizations over the same six years. The very category of spending that §4945's oversight rule is built to police was flowing through the conduit while, on the face of the filings, nobody was watching.

The recipients of the $101 million abroad are not named on the public returns — though Antar, in a discipline that defines the whole report, notes that this is not concealment. IRS instructions direct filers to leave those columns blank on the public copy. He says so plainly, the way an honest accountant flags the entry that cuts against his own thesis.

The Pattern in One Place

Any single one of these facts has an innocent explanation. Foundations fund §501(c)(4)s. Organizations outsource work. Charities run lean. Antar concedes every one of them, and that concession is what makes the whole thing land.

But all eight features, in one funding chain, with the same money, across the same six years, is a great deal of coincidence to ask a single structure to carry. A foundation that labeled its recipients noncharitable three times on one return, then moved $73.7 million to them. A principal recipient with zero employees in every year. Money in nearly equal to money out. Zero in every monitoring-fee category. Investment-management fees standing in for grant oversight that never appears. Unnamed foreign recipients. And $15 million in political contributions sitting downstream of it all.

Antar does not claim it was designed this way. A tax return does not disclose intent, and he refuses to pretend it does. What he does is read the documents, and ask the question a pattern like this is built to provoke: is there an innocent explanation for all of it at once, and where in the records would you find it?

That is the honest boundary of his analysis, and he draws it himself. The answer is not on the public returns. It lives in grant agreements, monitoring files, and board minutes that only an authority with subpoena power can pull. Which is precisely his point. You do not need to resolve anything about China to ask this question. You only need to read the filings — and then hand the rest to people with the power to demand the documents the public cannot see.

The findings, Antar reports, have already been referred to the Internal Revenue Service.

The Man Following the Documents

There is an irony in who is delivering this, and it is the kind of irony that makes the work more credible rather than less. The man explaining how to read a tax return for signs of a conduit operation is a man who once built operations the returns were designed to hide. Sam Antar spent the first half of his professional life defrauding the public and the second half teaching the government how he did it. He is a registered Democrat who has built his reputation on a single principle, which he repeats like a creed: follow the documents, not the politics.

In this case, the documents lead to a network whose politics happen to run hard in one direction. Antar treats that as irrelevant, and so should anyone reading him. The Internal Revenue Code binds every exempt organization in the country, regardless of what it advocates. A charity that moves $100 million abroad through an entity with no employees is either compliant or it is not, and that question is answerable without anyone agreeing about anything else.

The returns are still on file. The 2024 Form 990-PF still codes both recipients noncharitable in three separate places. Six years of People's Welfare Association filings still report zero employees, zero officer pay, and zero in every monitoring-fee category against more than $100 million moved abroad. The foundation's contractor schedules still name no one retained to watch where any of it went.

Anyone can read them. Sam Antar already has.

Read Sam Antar's full forensic investigation, with every figure tied to a specific form, schedule, and line, at WhiteCollarFraud.com.

This analysis is based exclusively on public records. Nothing in this report constitutes a legal conclusion. Where something is characterized as a documented fact, it is sourced to a primary filing. Where an inference is drawn, it is identified as such. The Unredacted follows documents, not politics.